Challenges remain for developers

News Credit To The Edge

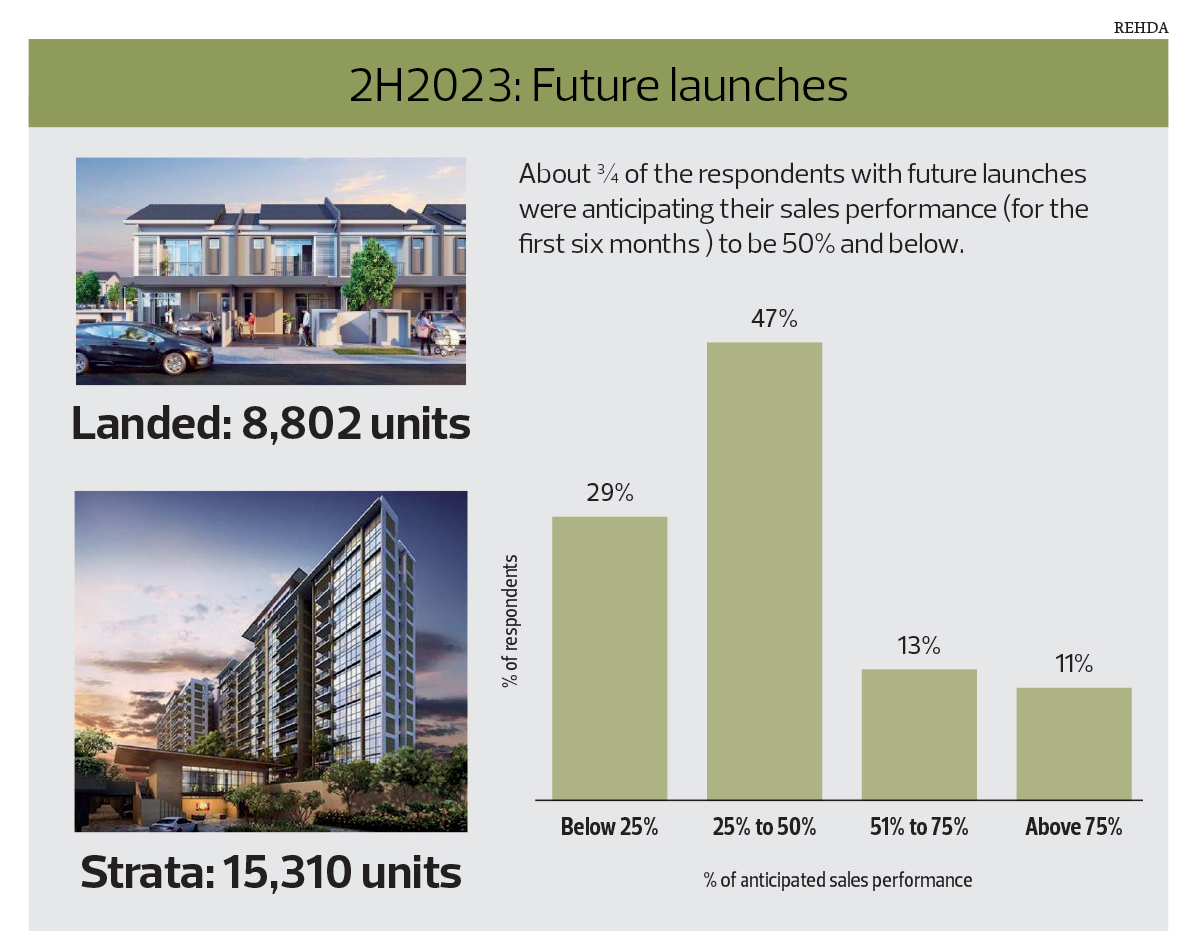

A survey of 188 property developers in Peninsular Malaysia by the Real Estate and Housing Developers’ Association (Rehda) Malaysia shows that about 53% of them plan to launch their projects in 2H2023, with three-quarters expecting to achieve sales of 50% or less after six months.

In a media briefing on the Rehda Property Industry Survey for 1H2023 and Market Outlook for 2H2023 and 1H2024 held on Aug 17, Rehda president Datuk N K Tong explained that the top reason for not launching projects in 2H2023 were unfavourable market conditions, business constraints and lack of suitable products or land bank locations.

Of the planned launches, there will be 15,310 stratified units and 8,802 landed. The price range for residential properties in Melaka, Perak, Penang, Kedah/Perlis and Pahang is between RM150,001 and RM300,000. Meanwhile, the price range for residential launches in Terengganu, Selangor and Kuala Lumpur is RM300,001 to RM500,000.

“There is a serviced residence project in Kuala Lumpur with 1,248 units at an average price of RM478,000 and an apartment project in Cheras with 1,453 units at an average price of RM340,000. Otherwise, prices in Kuala Lumpur won’t be [this low],” Tong said.

Negeri Sembilan’s residential launches are priced from RM500,001 to RM700,000, while Johor Baru’s are priced from RM700,001 to RM1 million.

According to the survey, about three-quarters of the respondents did not expect their sales performance for the first six months to be more than 50%.

“The unfavourable market condition is the perception of outlook [due to] the rising costs, the reality of house subsidies and so on. Developers know the pricing [but] they could have indications that the market is not ready for [the price range] yet. Something has to happen; either the [land or construction] cost comes down and/or affordability goes up,” Tong said at the Q&A session after the presentation of the survey.

“One consideration of the [anticipated sales performance] is the end-financing. There is a mismatch between banks’ loan growth targets and how much developers want to sell. Maybe banks will eventually [increase the growth target] but it won’t be in the next six months. If developers don’t see end-financing more forthcoming, they will be cautious [in launching].”

The survey also touches on rising costs, where the average increase in the cost of doing business is expected to be 15% in 2H2023, as opposed to 13% in 2H2022.

In 2023, some 87% of respondents observed a higher increase in building material prices in 2023 compared to previous years, with 51% increasing selling prices to tackle rising costs. Also, 48% of them reported a lower profit margin, and 43% used more cost-effective materials to address the issue.

On the outlook, 54% of the property developers were “neutral” and 22% were optimistic about business prospects in the second half of the year. More respondents (34%) were optimistic about business prospects in 1H2024.

1H2023 performance

Meanwhile, 53 respondents (36%) launched their projects in 1H2023, compared with 45 respondents (33%) in 2H2022. The total launched units increased by 53%. As for overall sales, 35% of the units sold were in new launches.

More than half (64%, or 8,998 units) of the new launches are stratified properties and the rest are landed properties. As such, the most popular property type launched was apartment/condominium (7,183 units), followed by 2- and 3-storey terraced homes (3,729 units) and serviced residences (1,223 units).

Nearly two-thirds (62%) of the new houses were priced at RM700,000 or below.

On sales, 36% of the respondents reported “better” performance compared to 2H2022, 26% indicated “no change”, 23% witnessed “worse” performance and 15% said no previous launches.

Of the respondents with “better” performance, 39% said the performance was better by up to 10%, another 39% said the performance was better by 10% to 20% and 22% said the performance was better by more than 20%.

Meanwhile, 53% of the respondents reported unsold completed residential units as of June 30, with the top reasons for these units being end-financing loan rejection (75%), unreleased bumiputera units (68%) and high pricing (51%). About half (47%) of unsold completed residential units were less than 12 months old.

The top three types of unsold completed residential units were apartments/condominiums (38%), serviced residences (28%) and terraced houses (20%).

At the same time, 28% of the respondents were at least optimistic about the property market and sales performance outlook in 2H2023, while more of them (38%) were optimistic for 1H2024. In terms of expansion in the next 12 months, 59% of the respondents indicated that they were looking at land bank expansion, and 52% expected capital expenditure (other than land).

Related News: